The amount of innovation in the insurance or insurtech space is accelerating and starting to be much more significant. We know that as entrepreneurs it’s uncanny to begin with the solution rather than the problem (believe me, we have plenty more posts reserved for that), but given the amount of interest we’ve been receiving we thought it may be better to give a taste of things to come. So, where do we begin?

Legacy systems in need of modernization

At the heart of every insurance carrier is a core system. Since these systems have not been updated for typically over 10 years, they’re now known as ‘core legacy systems’, it’s like going to buy a new house but then you realize that the plumbing is over 20 years old and if you want your awesome high pressure shower head, you have to replace the entire water piping (crude example, but something like that).

Then, at the heart of every core legacy system or in fact, every piece of software is the database where data is stored. So obvious and rudimentary, I know, so why revisit this. Well, because if you’re designing a hangman game vs. a complicated insurance product, it makes a huge difference. Making changes to a hangman game is rather simple, but making changes to an insurance product has many implications and knock-on effects and becomes complicated rather quickly from a software database design perspective, e.g. risk coverages, claims, proposals, billings, documentation, field items, etc.. etc…

In other words, if you make a small change, the likelihood of the rest of the system breaking drastically increases, thus that’s why insurers are very, very reluctant to change their systems — as the saying goes ‘if it ain’t broke, don’t fix it’.

Now, with the world changing as fast as it is, those systems must be replaced or insurers risk themselves becoming legacy (think DOS vs. Windows vs. now iOS & Android).

PolicyDock offers agility

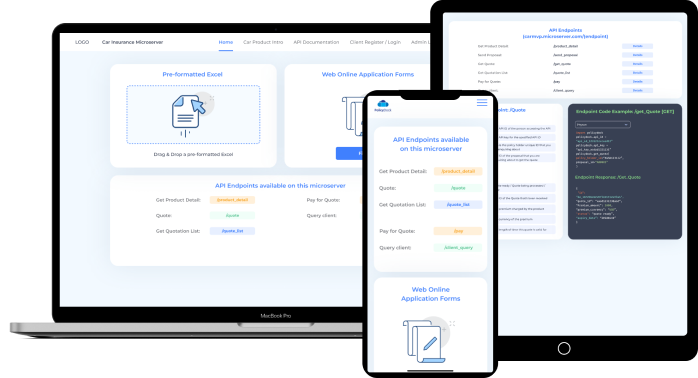

This is where PolicyDock starts, we’ve begun by tackling that problem: having a dynamic database model that’s easily updated with full versioning and can cater for nearly every single type of insurance product out there. This has taken years of work.

Then, looking at what software insurers use (which makes you feel you truly are back in 1995 half the time), we, of course, have specifically designed the system for the modern day, built cloud native to leverage the latest microservices architecture and infrastructure that is out there — AWS rings a bell. Of course, it’s cloud agnostic, i.e. choose your cloud vendor (AWS, Azure, Google Cloud etc…), we don’t mind. Most insurance systems today are hosted on-premise and are slowly moving to the cloud (check previous post…)

How long will it take to upgrade a legacy set-up?

As a client, your first thoughts and questions are probably ‘this sounds all fancy and great, but how long is this going to take?’ The answer is, we digitize any insurance product in a matter of DAYS, we wanted to have a radical approach that just basically puts the power of a full policy administration system up instantly in our clients’ hands for any type of insurance product. These systems typically cost insurers millions of dollars each year.

Moreover, we didn’t want our clients to be dependent on us (more on this coming in later posts), we wanted to think of our clients as our partners and vice versa, so we made the system totally modular and open via our API first approach with great documentation, while having data security and permissions fully interoperable with any other system and available to partners. In short, we want to empower our clients and let them choose their own digital destiny. After seeing a lot of innovation in insurtech in recent years, we simply cannot believe that a single vendor will be able to provide the best system to any one insurer.

You get all this in a powerful, white label online portal delivered faster, cheaper and remotely to anywhere for any jurisdiction — hence, Platform-as-a-Service (available today, ‘stocks always last’ 😊)